Article Text

Abstract

Equal access to vaccines has been one of the key ethical challenges during the COVID-19 pandemic. Most scholars consider the massive purchase and hoarding of vaccines by high-income countries, especially at the beginning of the pandemic, to be unjust towards the vulnerable living in low-income countries. A recent proposal by Andreas Albertsen of a vaccine tax has been put forward to remedy this problem. Under such a scheme, high-income countries would pay a contribution, conceptualised as a vaccine tax, dedicated to buying vaccines and distributing them to low and middle-income countries. Proceeding from this proposal, we critically assess the feasibility of a vaccine tax and suggest how to conceptualise and implement a vaccine tax in practice. We present our ‘VaxTax model’ and explore its comparative advantages and disadvantages while considering other possible measures to address the global vaccine access problem, also in view of future pandemics and disease outbreaks.

- COVID-19

- Ethics

- Health Care Economics and Organizations

This is an open access article distributed in accordance with the Creative Commons Attribution Non Commercial (CC BY-NC 4.0) license, which permits others to distribute, remix, adapt, build upon this work non-commercially, and license their derivative works on different terms, provided the original work is properly cited, appropriate credit is given, any changes made indicated, and the use is non-commercial. See: http://creativecommons.org/licenses/by-nc/4.0/.

Statistics from Altmetric.com

Introduction: on the need of equitable access to vaccines

The international community has committed to an unprecedented global vaccine roll-out to overcome the COVID-19 pandemic. The heads of state and governments of the G20 have committed in their Riyadh Declaration in November 2020 to ‘spare no effort to ensure [the] affordable and equitable access [to COVID-19 diagnostics, therapeutics and vaccines] for all people, […] recogniz[ing] the role of extensive immunization as a global public good’.1 In their 2021 Rome Declaration, they reaffirmed ‘that extensive COVID-19 immunization is a global public good’ and pledged to ‘advance [their] efforts to ensure timely, equitable and universal access to […] vaccines, therapeutics and diagnostics, with particular regard to the needs of low- and middle-income countries’.2 Similar efforts were declared by G7 countries at their 2021 summit in Carbis Bay, England,3 4 and by the World Health Assembly.5 As of May 2022, global vaccination rates are still far from the level required as part of an effective global pandemic response. As of 25 April 2022, only 65.1% of the world population and only 15.2% of people in low-income countries have received at least one dose of a COVID-19 vaccine.6 There is an urgent need to respond to the challenge that current global vaccination rates are insufficient to adequately tackle the COVID-19 pandemic, and to offer a scheme to ensure equitable access to vaccines. Such scheme may be useful for the ongoing pandemic, in case of new vaccines being released on the market (eg, specific for the COVID-19 Omicron variant) and for future pandemic preparedness. Also, this similarly applies to new public health threats, such as the ‘monkeypox’, and the public health response to the disease outbreak. While the international community has made remarkable efforts to ensure an improvement of vaccine supply in low and middle-income countries (LMIC) through the COVID-19 Vaccines Global Access (COVAX) facility,7–9 further steps are necessary to optimise global COVID-19 vaccination rates.

A vaccine tax: building on a recent proposal

Beyond existing schemes based on donations, such as COVAX, and proposals for patent waivers as instruments to improve global COVID-19 vaccination rates and access to vaccines in LMICs,7 10 the suggestion of a global vaccine tax has recently received considerable attention.11 Proceeding from Albertsen’s proposal,11 a vaccine tax has several advantages. First, it would likely favour a more equal distribution of vaccines, as a vaccine tax imposed and agreed on by purchasing states would likely ensure that more funds are allocated to LMICs. Second, as explained,11 this does not prohibit high-income countries from buying as many vaccines as they want and preserves their privileged position to purchase vaccines and protect their population. Depending on the taxation model, a tax can, however, operate as a disincentive. The vaccine tax should be generally progressive, and should not be intended to discourage or limit a national state’s ability to protect its population at large. Governments should thus minimise overexpenditures beyond population coverage for vaccines that are likely to not find any usage, will be discarded or become obsolete due to, for example, emerging variants. Importantly, both points are considerably different from donations: a vaccine tax would imply a tax scheme applied to every participating country equally. That is, countries that buy more vaccines would pay higher tax contributions. Second, different from donations that are unrelated to (eg, progressive) tax payments, a tax can disincentivise vaccine hoarding.

Finally, Albertsen points out that a vaccine tax would likely not impact companies’ ability to produce vaccines and be remunerative.11 It can thus avoid the challenge patent waivers are facing, that producing companies may no longer have incentives to be at the forefront of research, potentially impacting the world’s preparedness for future pandemics. For donations—yet another suggested approach to remedy the unequal distribution—there is no just and justified scheme to determine how much contribution should a state provide to COVAX, and donation schemes can potentially be abused for political purposes.7 In line with these considerations, a vaccine tax seems to be a plausible starting point to ensure equitable vaccine allocation globally.

Critical assessment of the current approach

In view of the above, we will critically assess Albertsen’s proposal and make suggestions for potential improvements and how to conceptualise and implement a vaccine tax. We shall explore the comparative advantages and disadvantages of a vaccine tax.

Tax sovereignty

Albertsen’s proposal of a vaccine tax is anchored in the idea that producers should collect ‘taxes’ from national states and act as super partes governing bodies regulating vaccine purchases and increase access to vaccines worldwide.11 We would like to clarify that from a legal viewpoint, taxes are imposed by national or local governments on citizens or legal entities. The idea of a private enterprise raising and collecting taxes on the products they produce is new and unlikely to work, as its implementation would require such companies to start playing a role in public health governance, which does not meet their expertise. Also, rather than speaking of a tax in the legal sense, some sort of ‘individual and voluntary contribution’ by firms might be a more appropriate notion in that model.

We suggest maintaining a chain of responsibilities in line with expertise and sovereignty: producers produce vaccines and national states purchase vaccines according to their needs and collect taxes. Since the vaccine tax would not be collected for domestic purposes but to buy and subsequently transfer vaccines to other countries, an internationally recognised governing body would further need to collect the ingested vaccine taxes from national states. The concept of such ‘international’ vaccine tax would still be innovative. So far, international taxation has referred to tax schemes developed by international bodies and implemented at the domestic level. For instance, the Organisation for Economic Co-operation and Development (OECD) has launched a framework for international tax reform with 130 participating countries to ensure that multinational enterprises pay a fair share of tax in the countries they operate.12 However, neither these enterprises nor OECD can finally act as sovereign entity to collect taxes. Tax sovereignty is assigned to governments. In the case of a vaccine tax, states could, however, commit themselves to transferring the collected taxes to a coordination body that furthermore uses the money to buy vaccines for LMICs.

So, if a ‘tax’—legal and terminological problems aside—would be self-applied by the vaccine producers, it is not evident why companies would commit themselves to paying taxes: any self-imposed tax makes them potentially less competitive with other international vaccine producers. So, it seems hardly plausible that companies would infringe themselves an extra fee. This position is backed up by past experiences of tax evasion and tax erosion by internationally operating companies.12 Moreover, since COVAX does not have any tax authority (as explained above), it also seems unlikely that vaccine producers would follow any suggested (non-binding) tax scheme.

Implementation

We argue that COVAX could be the institution using the collected tax money to buy and distribute vaccines, as suggested by Albertsen himself. COVAX has faced different critiques regarding its concept, implementation and management, which we will not address in any detail. Still, it is also worth noting that one of the initial weaknesses of COVAX was related to the small donations. The facility could design and push for a tax scheme and framework to precisely increase its fundings. Still, we recall that COVAX will not have tax sovereignty and thus relies on the voluntary agreement of countries to participate in a tax scheme and transfer the tax money to COVAX. A tax scheme, then, must be first and foremost subject to an international treaty or tax agreement, where countries self-commit to subject themselves to a tax framework and tax scheme. Yet, COVAX could take over the coordination of such agreement.

The main reason to think of COVAX as an institution managing tax revenues is owed to its mandate. COVAX has been established as a global collaborative to accelerate the development, production and equitable access to vaccines. COVAX is co-led by the vaccine alliance Gavi, the Coalition for Epidemic Preparedness Innovations, and WHO, which has helped the facility develop competencies in vaccine development, distribution and the management of funds (the revenue side). While it would be problematic if a private foundation had similar power, COVAX has the advantage to function as a public body to address the needs of governments. Thus, we argue that the facility is a well-suited candidate to steer a new scheme for a vaccine tax effectively. It is certainly true that COVAX itself could still be improved in terms of transparency, participation and legitimacy, as outlined in previous works,7 13 but this would not in principle rule out an expansion of its mandate when it comes to the design and implementation guidance for a global tax scheme.

Can a VaxTax model work in practice?

Having considered the idea of a vax tax and having defined how such a tax could be designed and by whom it should be collected, we proceed to evaluate whether the outlined VaxTax model could work in practice, and how. An important premise is that the model below is just one of several possible similar models, thus it would need to be adapted following discussions and negotiations between producers, states and COVAX. The tax should ensure that as many doses as possible are distributed to low-income countries and should rise with increasing purchases relatively to population size.

Our model is based on publicly available data showing the number of vaccine deals and vaccines bought by national states or international organisations, and COVAX, between May 2020 and November 2021.14 Estimates used in our model show that COVAX purchased or received between 2 and 3 billion doses. COVAX declares, as of May 2022, that they secured, optioned or received as donations 2.8 billion doses,15 16 and delivered 1.51 billion doses of COVID-19 vaccines as of May 2022.15 The biggest donor to COVAX is the USA, which announced and, so far, in part donated 900 million doses for COVAX, followed by the European Union (EU) with 526.6 million doses, Germany with 175 million doses (the EU accounts for about 1.1 billion doses if we also consider donations from individual states) and the UK with 100 million doses.16

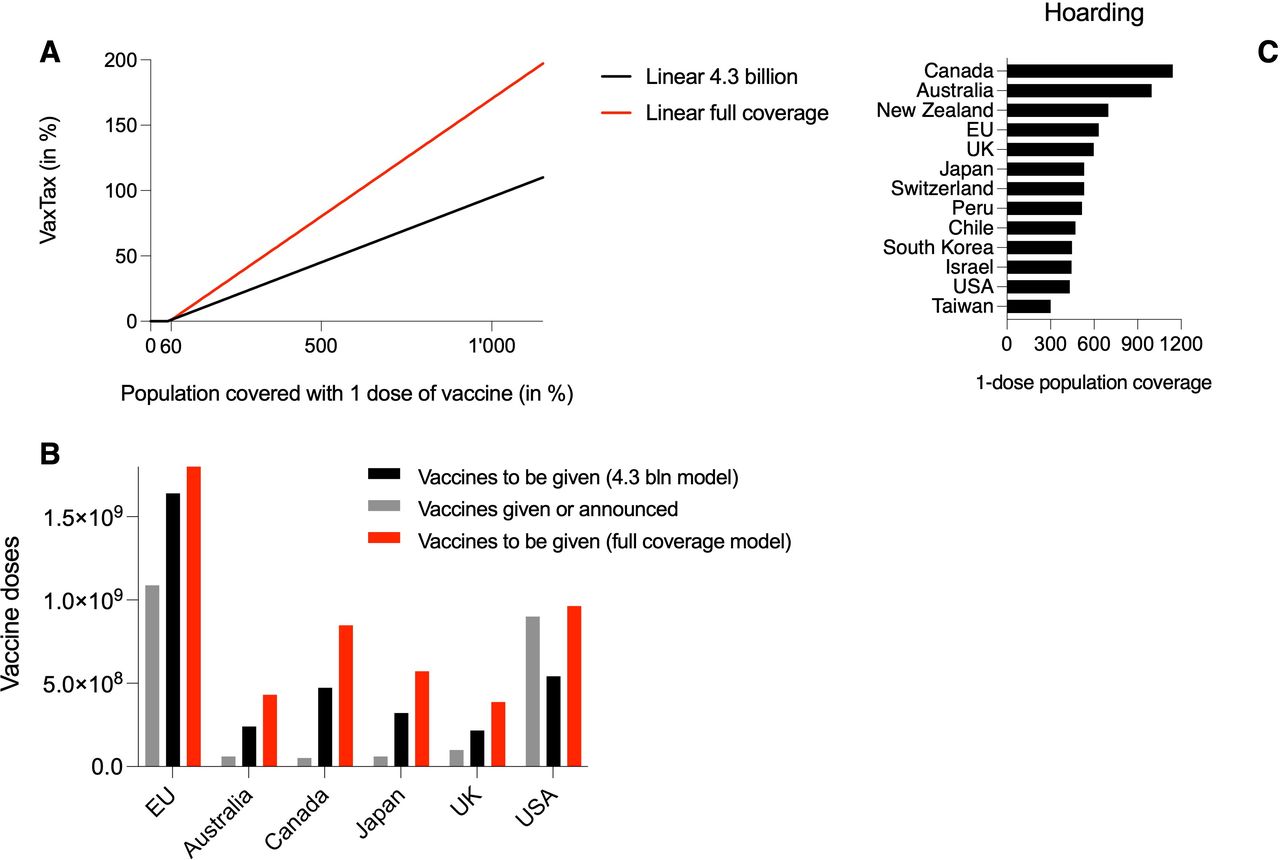

The curve which determines how the increase in taxation should be effectively designed may be subject of discussion. For simplicity, we envisage a tax scheme which linearly progresses with increased purchases relatively to population size. A scheme based on exponentially higher taxation levels is likely to be unpractical and unrealistic, and would likely be opposed by high-income countries. As shown in figure 1A, we envisage tax-free purchases of vaccines up to a coverage of 60% of the population, after which a very small tax incurs, and grows linearly up to 5% with a one-dose complete coverage of the population. This means that for 100 doses of vaccines purchased, the cost to buy five additional doses of vaccine would be given to COVAX in the form of a tax. Following this scheme, a two-dose full coverage of the entire population of a country would incur in a 15% tax. We assume such taxation, combined with the fact that vaccines are tax free until a 60% coverage, would not constitute a major burden for states; we also think this taxation burden will leave space for discussion and will be soft enough to prevent states to leave the negotiation table. The 60% coverage threshold is, we think, a reasonable example to start the discussion, but may be subject of negotiation; a lower percentage would likely result in lower compliance from states, and a higher percentage would result in less funds available for LMICs for access to vaccines. As per our scheme, a three times coverage of the population results in a 25% tax, a four times coverage in a 35% tax. Hoarding vaccines to cover the population 10 times would result in a 95% tax: for 100 doses of vaccines purchased, the cost to buy 95 additional doses would be paid to COVAX. According to our taxation scheme, states would have had to donate 4.3 billion doses during the COVID-19 pandemic, nearly double the number of doses received and purchased by COVAX. We have also added a second linear model which aims at reaching a one-dose full coverage of the world’s population, with a relative taxation scheme following a steeper slope (figure 1A). To reach 7.7 billion doses of vaccines donated to COVAX, the VaxTax would need to be of 8.2% for a 100% population coverage with one dose of the vaccine (vs 5% in our model to reach 4.3 billion doses), which increases to a 100% tax for a 610% coverage of the population (which corresponds to a 56% tax in our model targeting 4.3 billion doses) (figure 1A).

{kind=link}

VaxTax model in practice and vaccine hoarding statistics. We propose two different models for a progressive VaxTax, both following a linear function with a different slope. The first model could have achieved a 4.3 billion vaccine doses target for COVAX (black line) during the COVID-19 pandemic, whereas the second could have covered the entire world population with one dose of the vaccine (red line), without even considering vaccines bought by individual states directly from vaccine manufacturers. The tax linearly scales with increasing vaccine hoarding: for the 4.3 billion model it starts with a 1% tax for a 60% coverage of the population with one dose of the vaccine, and reaches a 109% tax for a 1140% coverage of the population. The full coverage (7.7 billion) model also starts with a 1% tax for a 60% coverage but reaches a 195.4% tax with a 1140% coverage of the population (A). According to our 4.3 billion doses model (black bars), the USA donated more doses than required, whereas the European Union (EU), the UK, Japan and especially Australia and Canada have donated very few doses (grey bars) compared with what our VaxTax scheme would require. The results are further exacerbated with our full coverage scheme (red bars), according to which only the USA, among the mentioned main players, donated a number of vaccine doses comparable with what our scheme would require (B). The main vaccine-hoarding countries are Canada (11.42 doses per inhabitant), Australia (9.96 doses), New Zealand (6.98), the EU (6.32), the UK (5.98), Japan (5.32), Switzerland (5.32), Peru (5.16), Chile (4.72), South Korea (4.48), Israel (4.45), USA (4.32) and Taiwan (3.01) (C). Data are obtained from publicly available data released by Launch and Scale Speedometer14: the number of vaccines hoarded has been calculated from the number of known vaccine purchases per country from each manifacturer, divided for the population size.

Our analysis focuses on the 4.3 billion doses taxation scheme. According to such scheme, the only high-income country that respected and went beyond the parameters is the USA, which allocated an excess of 358.5 million doses to COVAX. All other major high-income purchasing countries have contributed far less to COVAX in relation to the number of purchases relatively to population size, as figure 1B shows. It is worth noting that the EU, according to our VaxTax model, has a deficit of 551.06 million doses with COVAX, and the UK of 117.08 million doses. The EU has in fact hoarded vaccines, between May 2020 and November 2021, to cover its populations 6.32 times, which would result in our scheme in a 58% tax and 1.6 billion vaccines to be donated to COVAX versus 1.1 billion doses donated.17 Similarly, the UK has hoarded vaccines to cover 5.98 times its population, and should—according to our model—distribute 217.08 million vaccines to COVAX versus the 100 million vaccines donated. Other relevant states in this context are Australia, which donated 60 million doses instead of 240.5 million doses as per our tax scheme, Japan (60 million doses instead of 321.1 million doses) and Canada (51 million doses instead of 473 million doses) (figure 1B,C). It is worth noting that Canada tops the rank, with a potential ability to vaccinate each person 11.42 times, regardless of age (figure 1C), followed by Australia and New Zealand.

Discussion: clarifications and limitations

Herd immunity

The purchase of vaccines in our model is tax free until vaccines cover 60% of the population of a purchasing state, since most estimates consider herd immunity to require that 60%–70% of the population is protected to block the chain of transmission.17 For the COVID-19 pandemic, this set threshold for the VaxTax is representative, and could be changed if parties agree. However, we think this is a good starting level for introducing taxation, as the 60%–70% threshold for herd immunity represents a possible target to reach in future pandemics.

A model for the future

Our model is based on a retrospective analysis of vaccine deals and hoarding by states during the COVID-19 pandemic. This model has been developed as a potential starting point to evaluate how to handle future public health crises, in which there is an initial scarcity of preventive or curative medicines or devices. Albertsen’s idea, as well as the quantifications and clarifications we brought forward with our VaxTax model, should be seen as an attempt to increase global preparedness to future pandemics with agreeable, realistic and measurable strategies. Even though it is not possible to precisely predict the aetiology of future infective agents with pandemic potential, it is nonetheless possible to learn practical lessons from the ongoing pandemic which can be useful and applicable for future pandemics, too. It is worth mentioning that: (a) vaccines originally developed for the then circulating strain of SARS-CoV-2 do not protect from COVID-19 infection with the same efficiency when infection is caused by the Omicron variant, although boosters protect from hospitalisation and death18; (b) the pharmaceutical industry is currently busy producing specific vaccines for Omicron19 20; (c) Omicron-specific vaccines will need to be distributed after they have been approved for use. These aspects show that our model could be applicable to a real-world scenario sooner than later and could help in preventing excessive hoarding of Omicron (or other future variants)-specific vaccines and allowing for a fairer and more efficient distribution of vaccines to low-income countries. The same may apply to emerging public health threats, such as ‘monkeypox’, where future vaccination campaigns will potentially face the same distribution problems. We should also point to the fact that there should be an evolution of the tax over time, which is, for reasons of simplicity, not considered in our model. If a state buys large amounts of vaccines in times of high shortage, imposing a tax may be more effective and appropriate than in a phase of vaccine surplus. Also, modelling assumes that the utility of a vaccine will be stable, at least over a certain amount of time, and may thus oversimplify the highly dynamic situation of vaccine development for a moving target, such as in the case of new variants.

Open issues: allocation, infrastructure and vaccine hesitancy

While Albertsen clearly states that the implementation of a vaccine tax cannot improve global vaccine access alone, he claims that it could remedy the distribution problem.11 To give a fair picture of the actual problem, a vaccine tax can only improve vaccine funding. This is, of course, also a matter of pricing, and of the margins that are considered acceptable in a public health crisis. Yet, solving the revenue problem through a vaccine tax might increase the available funds for a more equitable global vaccine distribution, but does not tackle problems related to the equitable allocation of these funds. First, many poor countries face problems in implementing successful COVID-19 vaccination campaigns due to a lack of medical infrastructure. Allocation also requires that vaccines are accepted by the targeted population. The success of a vaccination campaign heavily depends on healthcare resources, infrastructure and the availability of trained healthcare staff.7 Second, vaccine hesitancy remains a major impediment to a successful global vaccination campaign, also in LMICs. Third, an equitable global vaccine distribution also depends on the foreseen allocation scheme. A needs-based global allocation, for instance, would consider the potential reduction of premature deaths as consequences of the health emergency, the overall economic improvements, as well as the extent of people being spared from poverty through the access to vaccines.14 21 In this respect, the chosen distributive scheme determines whether a distribution outcome is equitable and efficient. Last, a vaccine tax cannot replace efforts to build production capacities in LMICs, a necessary measure to increase the global vaccine supply and to improve access in the respective countries.7

Vaccine hoarding

A vaccine tax can do little to penalise vaccine hoarding in countries that do not participate in the proposed international tax scheme. At first, it seems that the richest countries would be least interested in implementing a scheme that imposes a considerable tax burden on them. Implementation might not succeed immediately but would take several rounds of negotiations, similar to climate agreements.13 However, one needs to consider that participants in a negotiation scheme aim to yield a net gain. Gains are not necessarily exclusively financial but can relate to reputation gains (or losses in case of non-cooperation) on the international stage. These gains or losses in reputation may compensate for potentially absolute financial gains or losses in the procurement of vaccines when taxes are implemented.8

A vaccine tax compared with alternative proposals

Albertsen points out that a vaccine tax will not radically rejig the current global system. For instance, a vaccine tax will only lead to a more equitable global funding scheme among participating countries, where richer states buying up more stocks finance more vaccines for the global poor.11 He understands that a vaccine tax will not touch the large profits reaped by vaccine producers that may also bear a moral obligation to contribute to a more equitable global vaccine distribution. Albertsen thus conceives his proposal as ‘piecemeal improvement of a system that is flawed in many ways’.11 We would like to analyse the advantages and shortcomings of a possible vaccine tax in the light of alternative measures. Starting with the advantages, one might ask what a vaccine tax can add to the existing system, where rich countries either donate vaccines to poor countries or commit themselves to transfer payments to the global access facility COVAX. We hold that a vaccine tax leads to a systematisation of vaccine funding and ensures that the burden of vaccine funding is more equitably distributed between all countries participating in such scheme. While vaccine donations have led to dependencies of LMICs from their donors, high-income countries joining COVAX only commit payments that, in turn, allow them to procure doses to vaccinate 20% of their population.7 This means, payments do not depend on the doses purchased outside COVAX. Hence, a vaccine tax would generally be more equitable, as it implies a greater financial burden on the countries that hoard vaccines. An elaborate tax scheme could moreover render contributions to COVAX more transparent if adequately institutionalised and controlled.

Alternatives like patent waivers and compulsory licences target producers directly. Under such measures, a government permits a local manufacturer to produce a product for domestic consumption without the patent owner’s consent. Such measures usually increase the number of vaccines available, decrease the profit of patent owners, but do often not improve the availability of vaccines in low-income countries if the necessary production capacity is missing.11 Still, patent waivers and compulsory licences arguably have a positive impact on the price, which itself improves the accessibility to vaccines in poorer regions of the world. However, these measures do not provide specific funding dedicated to the distribution of vaccines in LMICs per se and must be complemented by global coordination measures. A vaccine tax can indeed be a complementary measure to improve COVAX’s funding situation containing several synergic measures.

Conclusion

There is an urgent need to respond to the challenge that current global vaccination rates are insufficient to adequately tackle the COVID-19 pandemic. The VaxTax model proposed in this paper is based on the idea that the international community must undertake further efforts. This is in line with the idea brought forward by the United Nations that the COVID-19 global pandemic requires a global response based on unity, solidarity and multilateral cooperation.22 23

Ethics statements

Patient consent for publication

Footnotes

FG and FH are joint first authors.

NB-A and JWM are joint senior authors.

Twitter @fedgermani

FG and FH contributed equally.

Contributors FG and FH contributed equally. FG and FH wrote the paper. FG, FH, IO, NB-A and JWM edited and revised the manuscript. JWM and NB-A proposed the VaxTax model. FG practically established the VaxTax model. JWM is the guarantor.

Funding The authors have not declared a specific grant for this research from any funding agency in the public, commercial or not-for-profit sectors.

Competing interests None declared.

Provenance and peer review Not commissioned; externally peer reviewed.

Other content recommended for you

- Analysis of the institutional landscape and proliferation of proposals for global vaccine equity for COVID-19: too many cooks or too many recipes?

- Vaccine equity in COVID-19: a meta-narrative review

- It is not too late to achieve global covid-19 vaccine equity

- Reserving coronavirus disease 2019 vaccines for global access: cross sectional analysis

- Global access to COVID-19 vaccines: a scoping review of factors that may influence equitable access for low and middle-income countries

- Estimating deaths averted and cost per life saved by scaling up mRNA COVID-19 vaccination in low-income and lower-middle-income countries in the COVID-19 Omicron variant era: a modelling study

- COVID-19 vaccines and the pandemic: lessons learnt for other neglected diseases and future threats

- Addressing sociodemographic disparities in COVID-19 vaccine uptake among youth in Zimbabwe

- Managing the challenges associated with decreasing demand for COVID-19 vaccination in Central and West Asia

- Comparing research and development, launch, and scale up timelines of 18 vaccines: lessons learnt from COVID-19 and implications for other infectious diseases